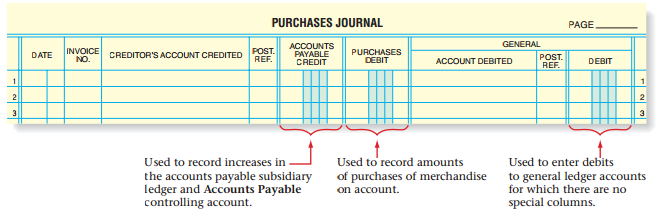

The purchases journal lists all credit purchases of merchandise. Entries in this journal usually include the date of the entry, the name of the supplier, and the amount of the transaction. Some companies include columns to identify the invoice date and credit terms, thereby making the purchases journal a tool that helps the companies take advantage of discounts just before they expire. The purchases journal to the right has only one column for recording transaction amounts. Each entry increases (debits) purchases and increases (credits) accounts payable. The number and the purpose of the special columns provided in the journal depend upon the nature of the business and the frequency of the purchases of the various assets.

For each transaction recorded in the purchases journal, the credit is entered in the Accounts Payable Credit column. The Purchase Debit column is for merchandise bought for sale. The Sundry Account Debit column is used to record purchases on account of items not provided for in the special debit columns. The title of the particular account is entered in the Account Title column and the amount of the debit is recorded in the Amount column. The number of the account is written in the Post Reference column at the time of posting.

For each transaction recorded in the purchases journal, the credit is entered in the Accounts Payable Credit column. The Purchase Debit column is for merchandise bought for sale. The Sundry Account Debit column is used to record purchases on account of items not provided for in the special debit columns. The title of the particular account is entered in the Account Title column and the amount of the debit is recorded in the Amount column. The number of the account is written in the Post Reference column at the time of posting.

Figure 1-1

The Purchase Journal

Recording the Purchase of Merchandise on Account

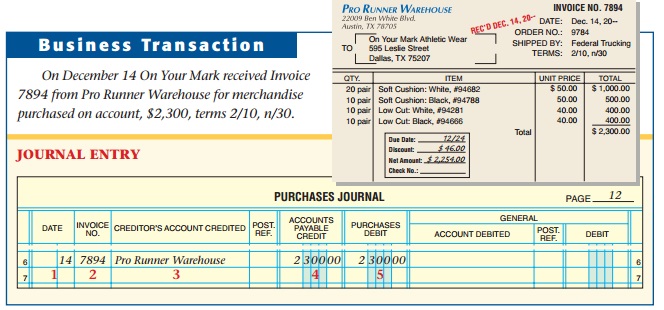

After verifying an invoice, the accounting clerk records the purchase in the purchases journal. Refer to the purchases journal and follow these steps:

- Enter the date in the Date column; Use the date the invoice was received, not the date the invoice was prepared.

- Enter the invoice number in the Invoice Number column.

- Enter the creditor’s name in the Creditor’s Account Credited column.

- Enter the total of the invoice in the Accounts Payable Credit column.

- For purchases of merchandise on account, enter the total amount of the invoice in the Purchases Debit column.

Posting from the Purchases Journal

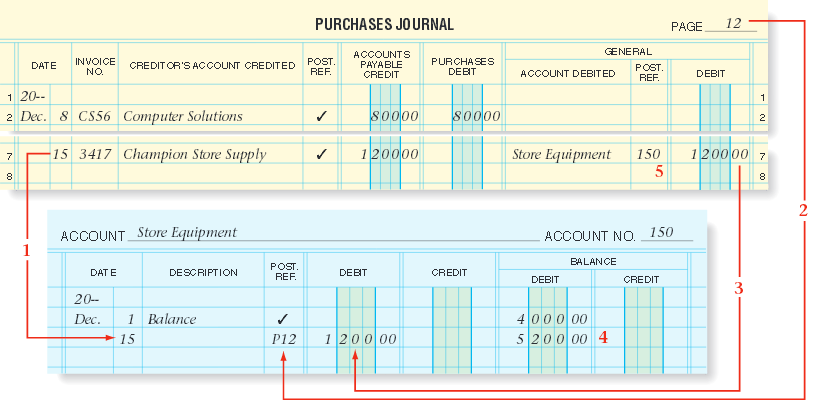

As you have learned, special journals save time in recording and posting business transactions. Each transaction in the purchases journal is a purchase on account. Therefore, each transaction is separately posted daily to the accounts payable subsidiary ledger to keep creditor accounts current.

Figure 1-2

Posting from the Purchases Journal

Refer to Figure 1-2 as you read about posting to the accounts payable subsidiary ledger.

- In the Date column of the subsidiary ledger account, enter the date of the transaction.

- In the Posting Reference column of the subsidiary ledger account, record the journal letter and the page number. P is the letter used for the purchases journal.

- In the Credit column of the subsidiary ledger account, enter the amount owed to the creditor.

- Compute the new account balance by adding the amount in the Credit column to the previous balance amount. Since there was no previous balance in Pro Runner’s account enter $2,300 in the Balance column.

- Returns to the purchases journal and place a check mark in the first Posting Reference column (next to the Creditor’s Account Credited column).

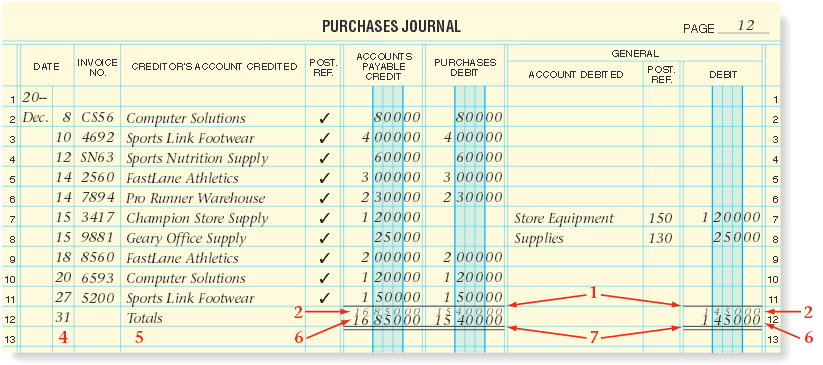

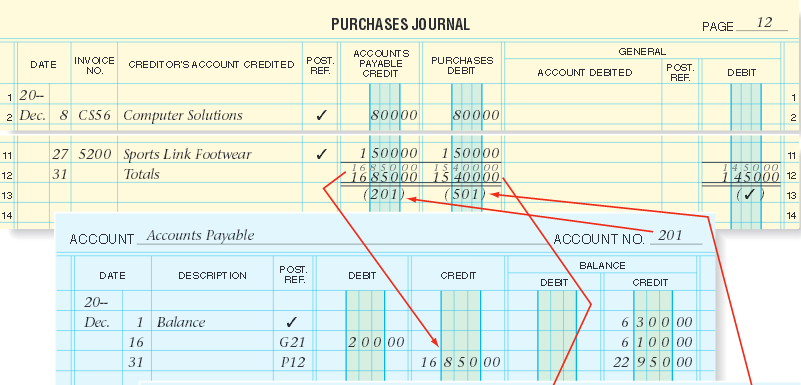

Totaling, Proving, and Ruling the Purchases Journal

To complete the purchases journal, refer to Figure 1-3 and follow these steps:

The completed purchases journal is a quick reference tool for the accountant to review current transaction that affect the PURCHASES account and the ACCOUNTS PAYABLE account.

- Draw a single rule across the three amount columns: Accounts Payable Credit, Purchases Debit, and General Debit.

- Foot each amount column.

- Test for the equality of debits and credits.

- In the Date column, on the line below the single rule, enter the date the journal is being totaled.

- On the same line, write the word Totals in the Creditor’s Account Credited column.

- Enter the three column totals, in ink, just below the footings.

- Draw a double rule across the three amount columns.

The completed purchases journal is a quick reference tool for the accountant to review current transaction that affect the PURCHASES account and the ACCOUNTS PAYABLE account.

Figure 1-3

The Completed Purchases Journal

Posting the Special Column to the General Ledger

Figure 1-4

Posting Column Totals from the Purchases Journal to the General Ledger

After totaling and ruling the purchases journal, the clerk posts the totals of the Accounts Payable Credit column and the Purchases Debit column to the general ledger accounts. Then the clerk calculates the new balance for each account and enters the new balance in the appropriate Balance column.

References

- Principles of Accounting, Baguino et. Al

- Century 21 Accounting. Ross, Hanson, Gilbertson, Lehman & Swanson. 6th edition

- http://www.accounting-basics-for-students.com/accounting-journals.html

- http://mrhaworth.weebly.com/uploads/2/8/0/8/2808974/glencoe_accounting_chp17.pdf

- http://www.cliffsnotes.com/more-subjects/accounting/accounting-principles-i/subsidiary-ledgers-and-special-journals/special-journals