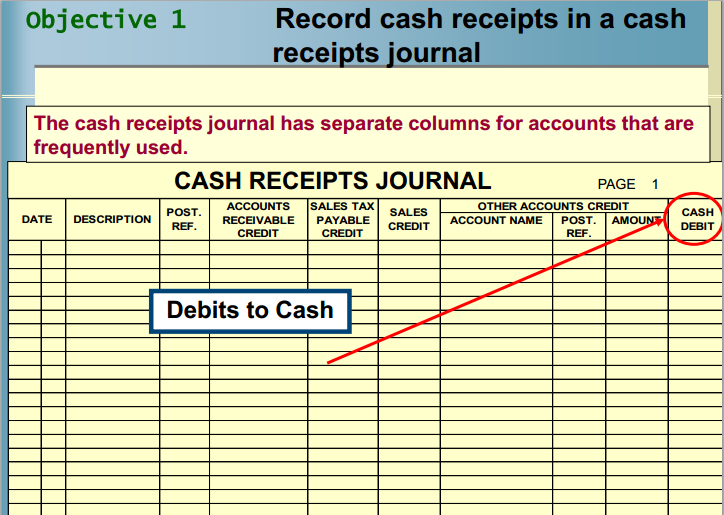

Designing a Cash Receipts Journal

- Date Column

- Account Credited or Other Description Column

– If a cash sale, use the description Cash Sale

– If cash is received from entering a loan agreement, specify the account credited as Loan Payable, use the Other Accounts column

– If cash is received from sale of fully depreciated equipment, specify the account credited as Gain on Sale of Equipment, use the Other Accounts column

- Posting Reference Column

– Dash indicates that all amounts will be posted as a column total

-- Account number in the Posting Reference column indicates that the transaction in the Other Accounts column have been individually posted to the applicable account.

- Provide separate columns for more frequent transactions, use the Other Accounts column for less frequent transactions, normally individual columns would be considered for the following accounts, if applicable.

Debit columns Credit columns

Cash Accounts Receivable

Sales Discount Sales

Credit Card Expense Other Accounts

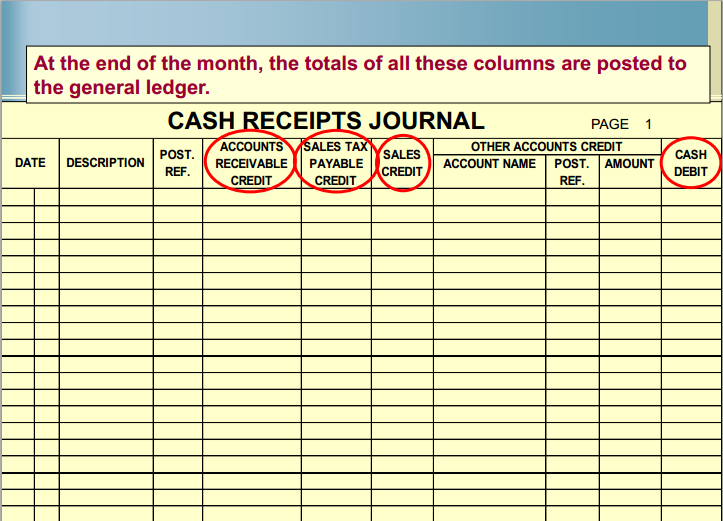

- Provide a summary of all debits and credits in lower right area of the Cash Receipts Journal with formulas using the columnar totals, then record the transactions and continue to check after each one is posted that the difference between the debits and credits is 0.

Posting the Cash Receipts Journal

The individual amounts in the Accounts Receivable column are posted immediately after journalizing to the ledger in order to keep the customers’ balances current.

The totals of Cash (debit), Sales Discount (debit), and Account Receivable (credit) and Sales (credit) columns are posted at the end of the month to their respective general ledger accounts. Their account numbers are also written below the totals to indicate that posting is completed.

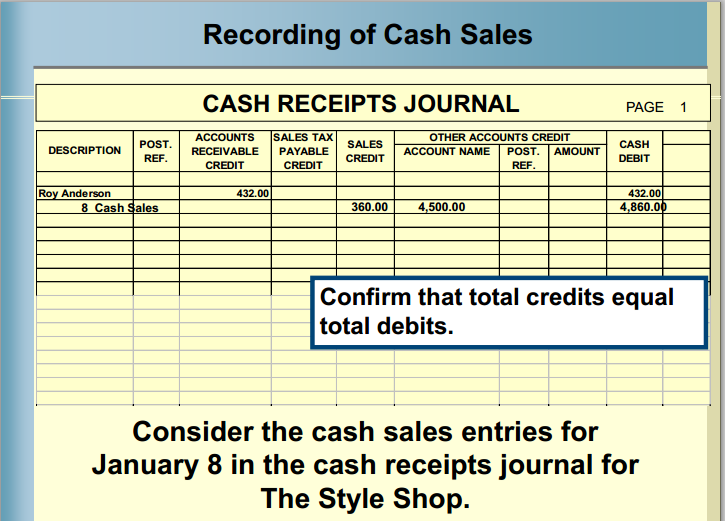

Cash sales are defined as sales in which the buyer's payment obligation to the seller is settled on delivery, for example by payment in cash or by debit or credit card. Sales via the internet paid by credit card and mail order sales settled on collection of the goods from the post office are examples of sales that fall under the definition of cash sales. The Bookkeeping Act sets strict requirements for documentation of cash sales.